Six Things I Took Away from Zonda FrameJune 08, 2026A rollercoaster market, resilient fundamentals, and a call to stop selling on incentives alone — here's what the data said.I recently attended the Zonda Frame session for the Houston region, and walked away with a clearer picture of a market that is, by almost every measure, holding up better than it gets credit for — while carrying real risks that deserve careful watching. The data was dense, candid, and worth unpacking for anyone working in or adjacent to new home development in Houston. Here are the six things that stayed with me.

1. Houston is outperforming — but the "rollercoaster" is real

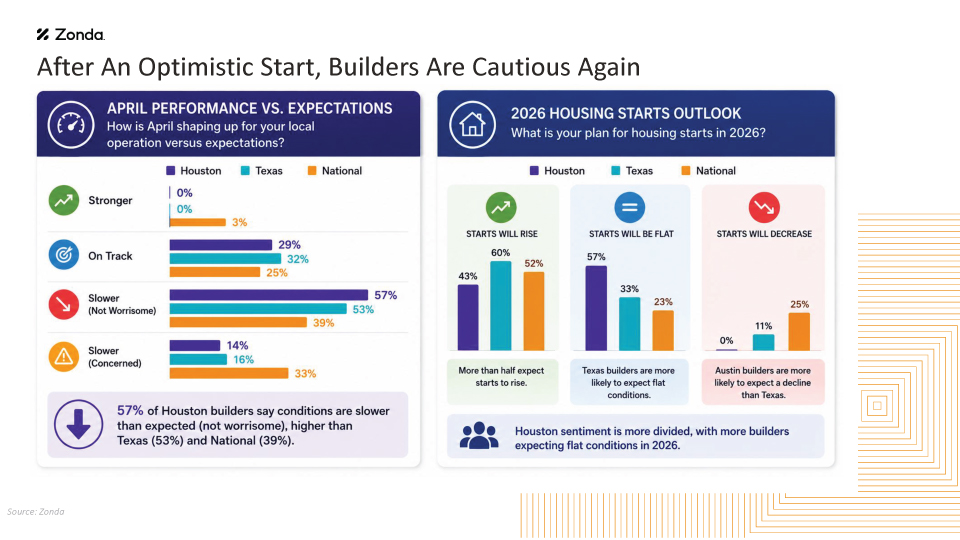

Source: Zonda The word builders kept using to describe this market was "rollercoaster," and the data backed it up. Sentiment starts strong, traffic picks up, then a headline out of Washington or an international flash point knocks it back down. That pattern has repeated itself through the first half of 2026.

Source: Zonda Even so, perspective matters. Start activity across the top 25 U.S. markets fell about 15% on average over the past year. Houston's decline? Six percent. When you put that next to Austin's 15% drop and Dallas's near-18% decline, Houston's sideways chug looks a lot more like stability than stagnation. And the market still holds the number two position nationally by volume.

2. Job growth is the number to watch — and it's worrying

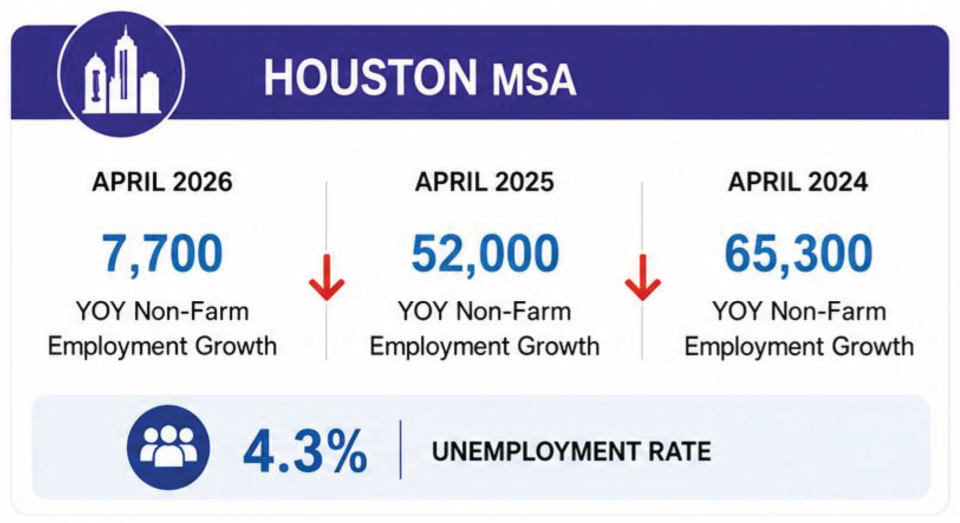

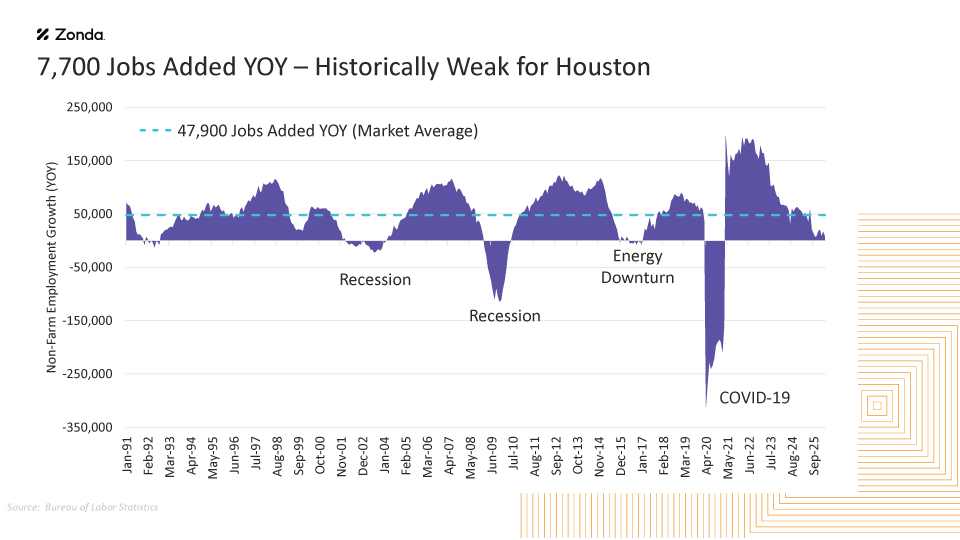

Source: Zonda Houston has historically added about 48,000 jobs per year. Over the past 12 months, that number was 7,700. That's a staggering shortfall, and it sits at the center of almost every demand-side challenge the market is facing right now.

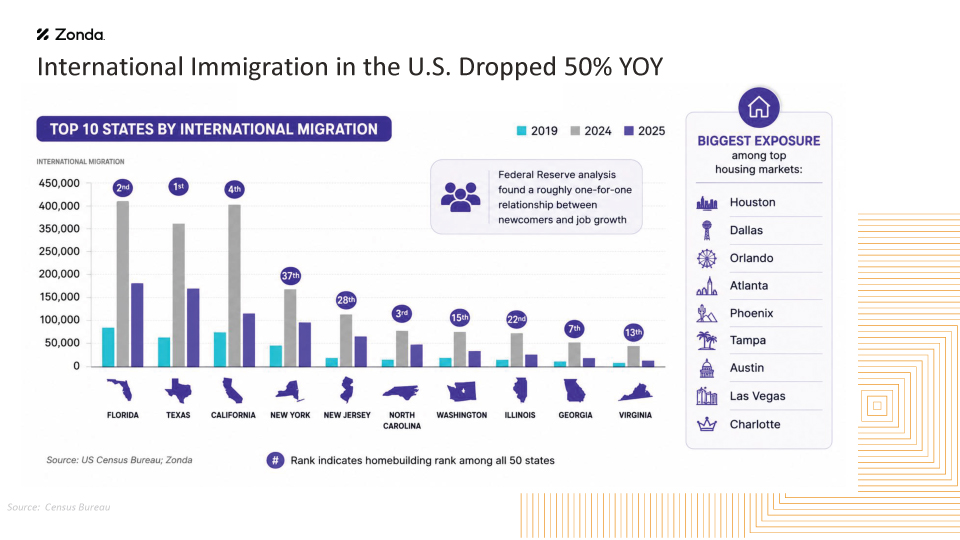

Source: Zonda The labor market is, as Zonda described it, "no hire, no fire" — unemployment remains low, but the hiring engine that normally drives household formation has stalled. International migration, which historically accounts for roughly 35% of Texas's net in-migration, dropped by half over the past year, compounding the problem since every migrant arrival has historically correlated roughly one-to-one with job creation.

Source: Zonda

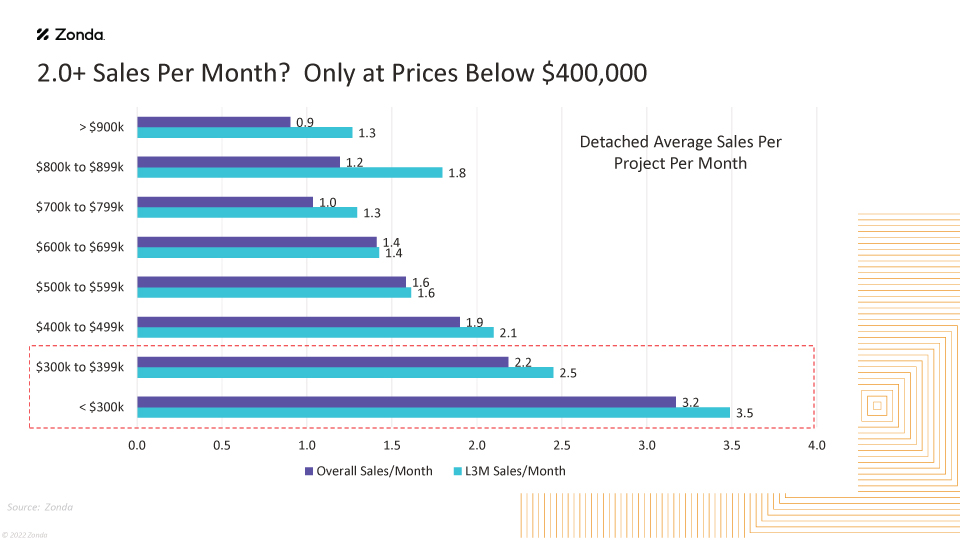

3. The market has bifurcated — and the math is different on each sideThe average sales rate across detached new home communities in Houston is about 2.2 homes per month. That sounds fine until you remember that the historical range has been 2.5 to 3.5. "Two is the new three," as it was put in the session — deals are being underwritten accordingly.

Source: Zonda But that 2.2 average masks a sharp split. On the value side — price points below $400,000 — builders are running 3 to 4 sales per month by sacrificing margin. On the luxury side, above $800,000, communities are holding closer to 2 sales per month with margins intact. The middle is the hardest place to be right now. "Two is the new three. We used to underwrite deals at three sales per month. Now we're zeroing out at two."Zonda Frame · Houston · May 2026

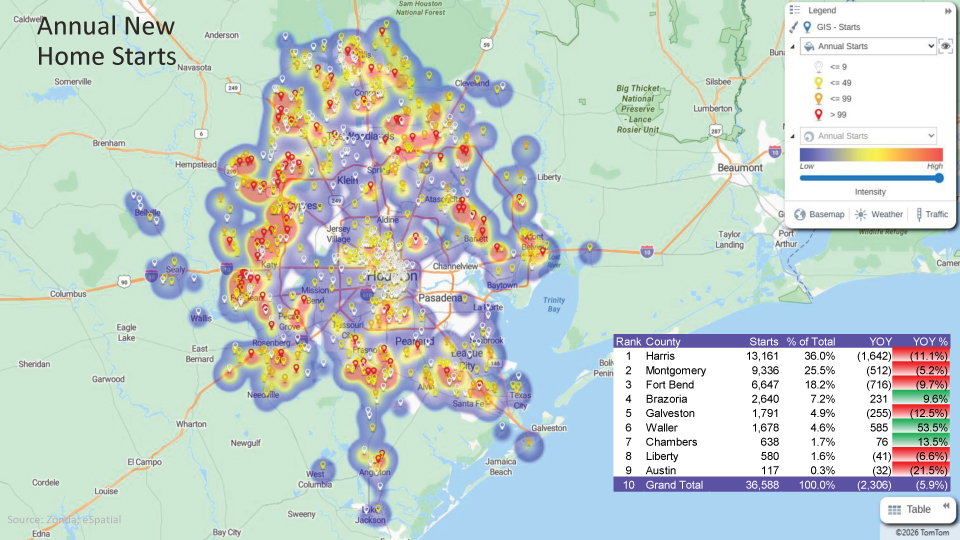

Source: Zonda Geographically, the strongest activity is concentrated around Crosby, Fulshear, Rosenberg, and Tomball. Montgomery and Magnolia — high-quality development areas that have attracted significant new supply — are becoming more competitive. Waller County stood out with 54% year-over-year growth in starts.

4. Inventory metrics look manageable — but the cushion is thinFinished vacant inventory sits at about 6,600 units, which represents 2.2 months of supply. That is still within the acceptable 2-to-3-month range, but it is near a record high on an absolute basis. If closing activity softens, that two months can become three quickly. The lot supply picture carries more long-term concern. The market has crossed above 24 months of lot supply — the upper edge of what's considered equilibrium. Even as builders have pulled back on starts, developers have kept delivering lots: nearly 12,800 in the first quarter alone, the highest first-quarter delivery pace since 2018. With another 14,000 lots actively under development and 27,000 more still in earlier pipeline stages, the imbalance between lot supply and absorption is real and likely to persist through 2027.

5. New communities are still succeeding — execution is the differentiator

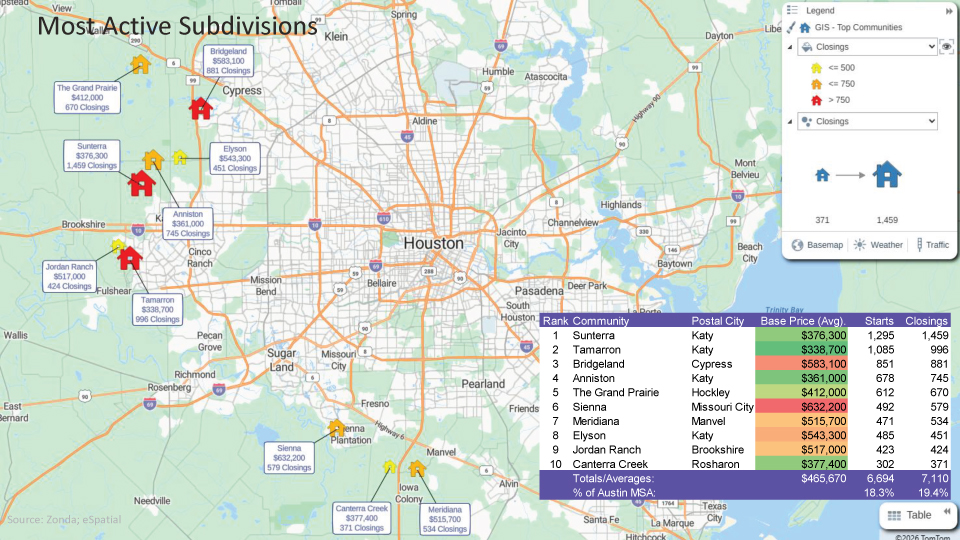

Source: Zonda One of the more encouraging data points from the session: Zonda tracked ten large-scale communities (all 1,000+ lots) that launched since early 2025. Eight of them have already surpassed 100 starts. Three —Grange by Johnson Development, and Synova and Sila (both by Lennar) — have crossed 100 closings in less than a year. The top-ranked community in the Houston market, Sunterra on the west side, logged nearly 1,500 closings over the past year. Three of the top four communities in the entire state of Texas are Houston-area projects. The demand is there. What converts interest into closings is location, school district, amenity delivery, and developer execution — not incentives alone. 6. The strategic imperative: stop selling transactions, start selling belongingPerhaps the most pointed message from the session, and the one I found myself thinking about most on the drive home: builders have been trained by the current market to compete on incentives — rate buydowns, price cuts, closing cost assistance. That's been necessary. But it's also conditioned buyers to treat new homes like commodities, evaluating each purchase against a checklist of financial concessions. The recommendation was to start moving back toward emotional connection: the neighborhood, the community identity, what daily life actually looks like in that development. The buyers are still out there. Consumer confidence is fragile, but it can also reverse quickly — the same sensitivity that pulls buyers off the fence can put them back on it when conditions improve. Builders who have built genuine community identity will be positioned better than those who have simply competed on price when that happens.

The bottom lineZonda's forecast for Houston: flat to 5% start growth for the balance of 2026, with meaningful choppiness month-to-month. The market is not broken — it's normalizing after an extraordinary run, and it's doing so more gracefully than most of its peers. But the margin for error is thinner than it has been, the lot pipeline is longer than comfortable, and the demand engine needs job growth to fire back up in order to sustain anything beyond sideways. For those of us thinking about how to connect with buyers in this environment, the data is a useful reminder that the fundamentals are still intact. The buyers exist. The equity is there. The emotional case for homeownership — community, stability, identity — hasn't weakened. What's fragile is confidence, and confidence responds to the story you tell as much as the rate you offer.

Author: Michelle LeBlanc, CEO | Marketing Strategy, Blue Sky Marketing |

Explore our Blog

Sign up for email updates!

Join over 3,000 other marketing professionals to learn how to improve and advance your company's marketing.

The Archives

- JULY 2026 (3)

- JUNE 2026 (1)

- FEBRUARY 2022 (1)

- DECEMBER 2021 (1)

- SEPTEMBER 2021 (1)

- AUGUST 2021 (1)

- JULY 2021 (1)

- JUNE 2021 (1)

- APRIL 2021 (1)

- FEBRUARY 2021 (2)

- DECEMBER 2020 (1)

- SEPTEMBER 2020 (1)

- AUGUST 2020 (1)

- MAY 2020 (1)

- JULY 2019 (1)

- AUGUST 2017 (1)

- JUNE 2015 (1)

- MARCH 2012 (1)

- AUGUST 2010 (1)